Aberdeen Municipal Income Fund is positioned to help investors pursue attractive, tax-exempt income in a resilient municipal bond market supported by strong credit fundamentals and compelling relative value. In this CEF Insights conversation, Mike Taggart and Miguel Laranjeiro discuss how Aberdeen's active, research-driven approach combines macro insight, bottom-up credit analysis, high-yield municipal opportunities, and prudent leverage to seek sustainable income over time. Learn why the fund may be well positioned for income-focused portfolios.

Transcript

CEFA:

Welcome to CEF Insights, your source for closed-end fund information and education brought to you by the Closed-End Fund Association. Thank you for joining us as Mike Taggart and Miguel Laranjeiro of Aberdeen Investments discuss the municipal bond fund market. Mike is Aberdeen's Head of Closed-End Fund Investor Relations. Miguel is Investment Director and Portfolio Manager for Aberdeen Municipal Income Fund, ticker symbol MFM.

Mike Taggart:

Okay, thank you everyone for taking the time to learn about the Aberdeen Municipal Income Fund, ticker MFM. Aberdeen recently became the investment advisor for MFM, which is a much larger fund than it was under previous management due to other funds being merged into it. The board has already increased MFM's monthly distribution by 25% in mid-June. The fund now pays 3 cents per share per month. And because of all these changes, I thought it would be appropriate to have Miguel discuss the municipal market, the team's investment approach, and the fund itself. Miguel, thanks for taking the time.

Miguel Laranjeiro:

Thanks, Mike.

Mike Taggart:

Yeah, let's start with the big picture and then work our way down to the fund level. So what are the key macro forces affecting muni credit fundamentals right now and market technicals?

Miguel Laranjeiro:

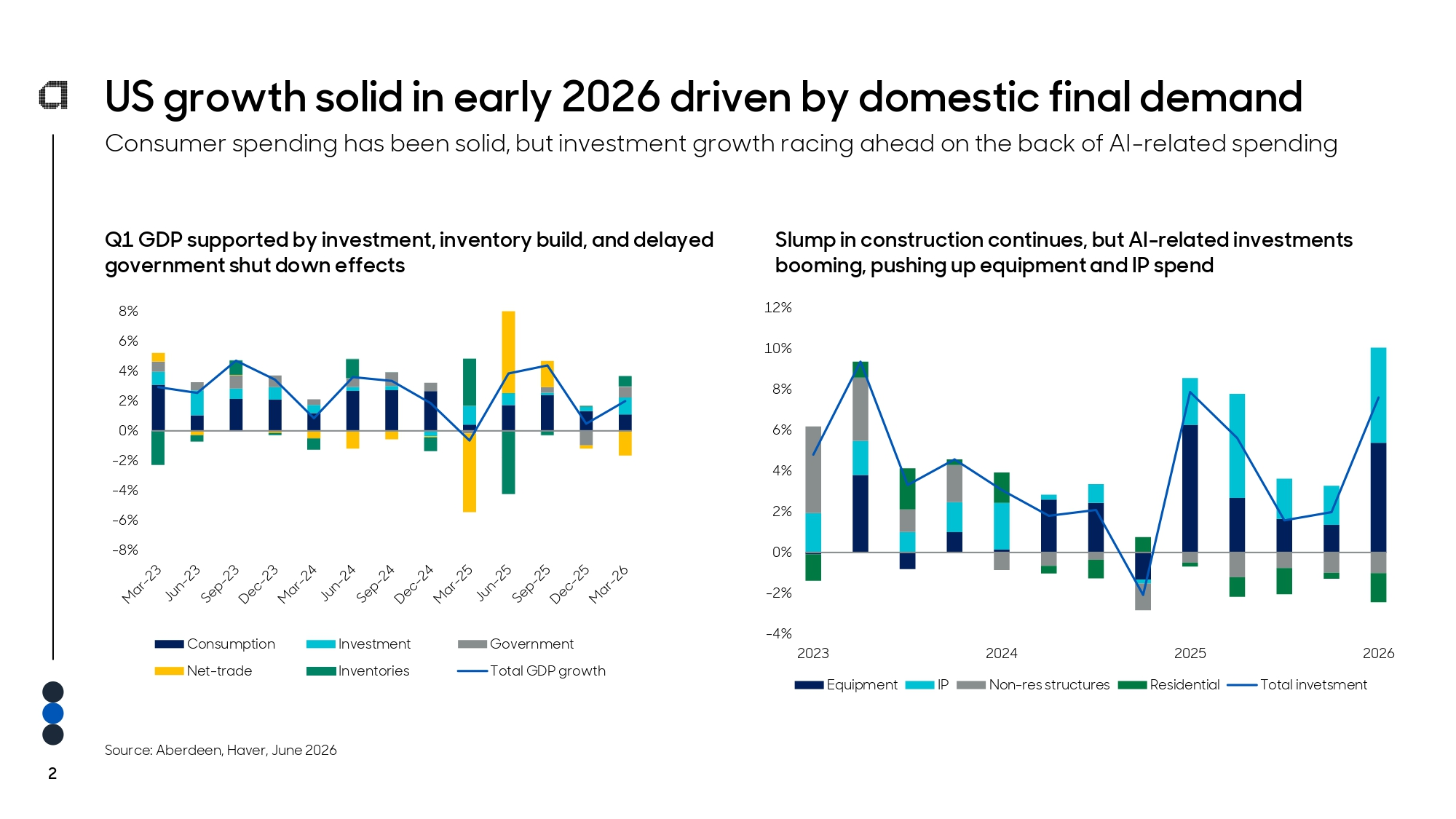

Yeah, so the economy has been really resilient despite the geopolitical tensions in the Middle East. We've seen the consumer continue to spend, perhaps not quite at the pace as they spent in 2025, but a solid consumer, no doubt. And we've seen the economy supported by macro tailwinds and AI CapEx spending, which has been supportive of economic activity for both state and local revenue collection. So, the backdrop fundamentally looks really solid from a technical-- from a fundamental point of view in terms of the health of the economy. And that's going to affect the Fed trajectory.

Mike Taggart:

And so, I mean, obviously the Fed trajectory in terms of the rates, municipal rates tend to kind of track that, right? But they're not identical. You know, what does the underlying economy say about kind of state revenues and that would affect municipal bonds?

Miguel Laranjeiro:

Well, tax collections are up year over year. Some of that is because of the inflationary influence that we've had from geopolitical tensions, everything costs more to do, costs more money to do. So, state coffers and local coffers are benefiting from that and reining in additional tax dollars for every dollar spent. So, what we've seen is a continuation of productivity in terms of state and local revenue collections. We've seen rainy day funds stay at fairly close to all-time highs. So, a really resilient market in terms of, you know, the muni market and the credit fundamentals.

Mike Taggart:

Okay, excellent. So, with that backdrop then, how have municipals been performing? You know, what have their returns been like?

Miguel Laranjeiro:

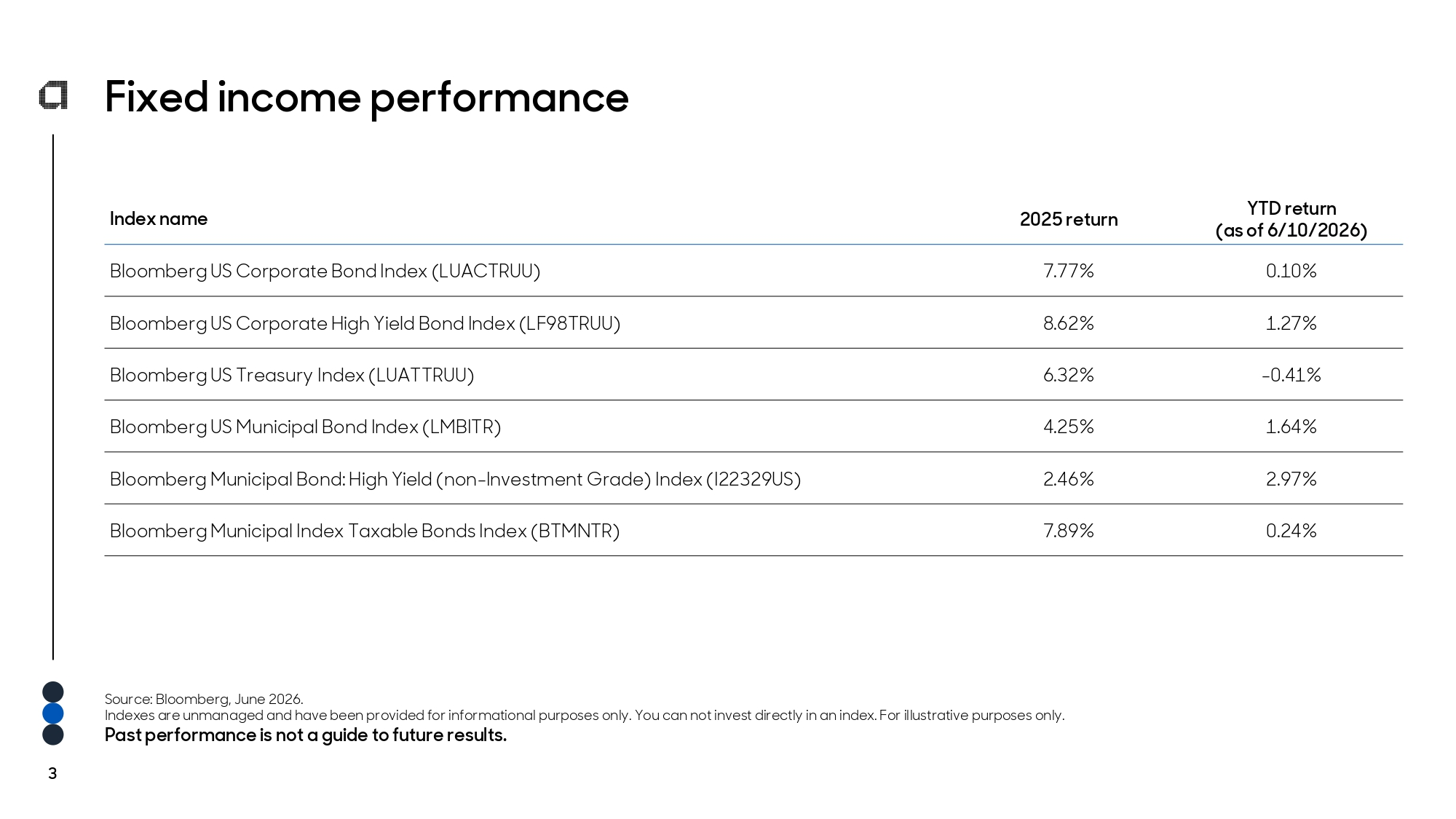

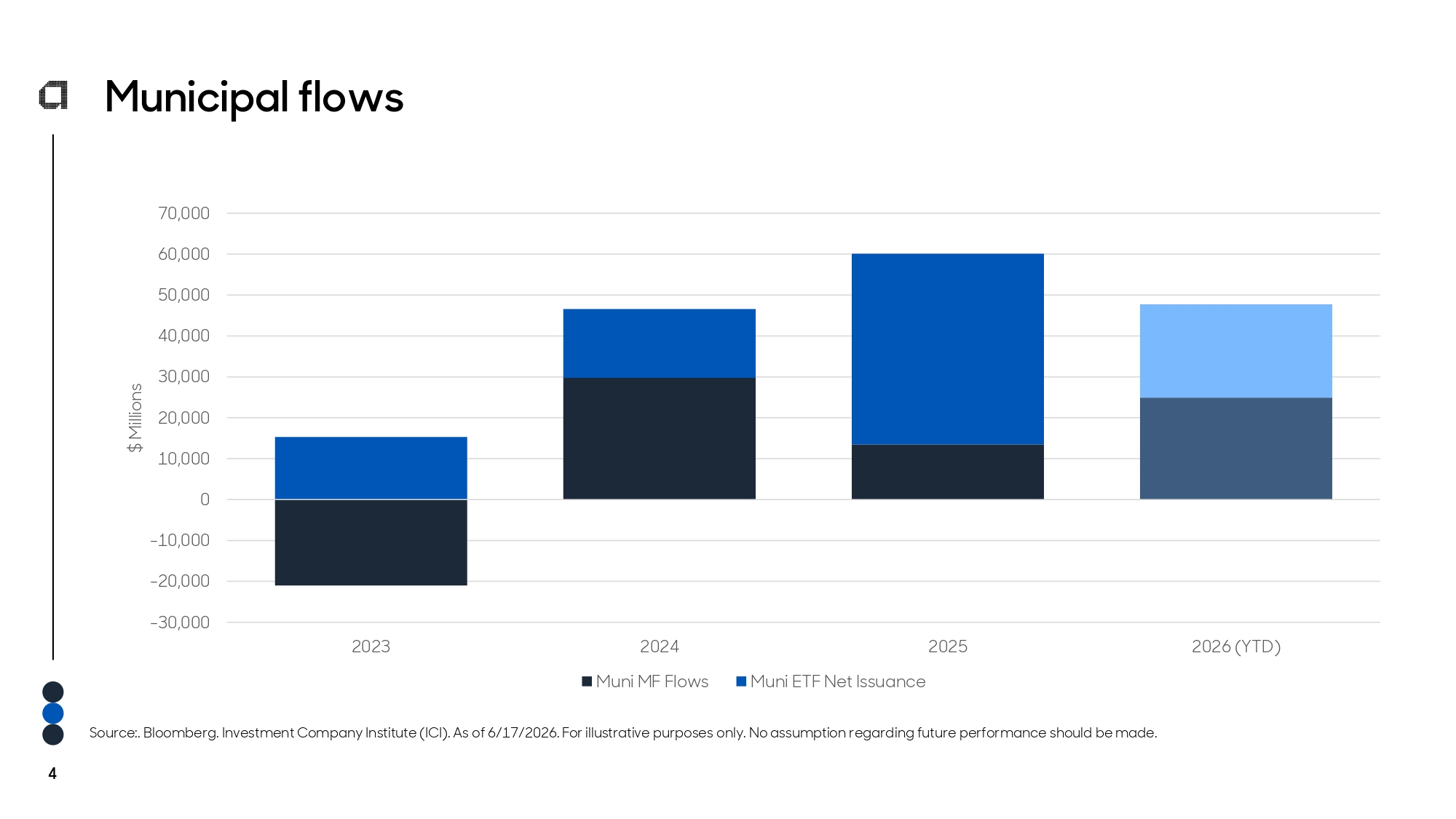

So, municipals have been performing well this year. Last year, they were one of the more underperforming asset classes in 2025. Some of that was really due to flows. The technical backdrop was negative for municipals, but fundamentally it's been in a good place. What we've seen in 2026 is investors are starting to take notice of the high absolute yields that can be had in the tax-exempt muni market. So, we've seen record setting inflows come into the muni market, and that has led into really outperformance of municipals overall. We've seen outperformance in high yield relative to their corporate high yield counterparts. And likewise, we've seen outperformance in investment grade relative to their investment grade or treasury counterparts. And a lot of that is due to the technical backdrop. We've seen a ton of capital flow into the municipal market, which has been supportive of what we've seen on the other side is record setting issuance for the third year in a row. We've seen record setting issuance in the municipal market.

Mike Taggart:

And so, you know, municipal investors typically are interested in, obviously yield, tax exempt yield, right? And so, with all these, with the good fundamentals behind it, behind the municipal market. I mean, wouldn't that argue that yields have come should come down because they don't need to, have such a high yield or, you know, how does that compare to kind of other fixed income?

Miguel Laranjeiro:

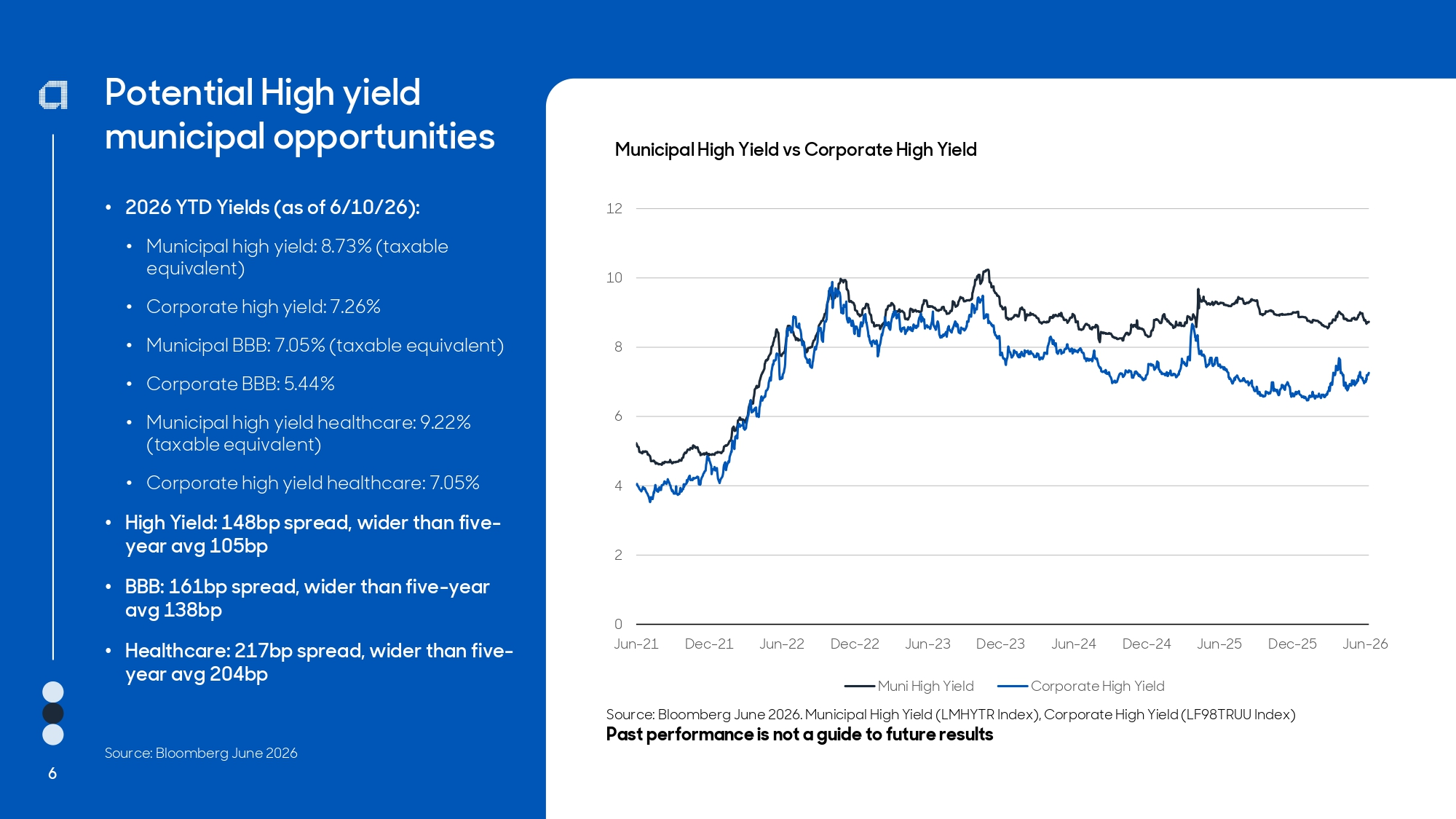

Yields still look attractive. Like I said, munis have outperformed other fixed income asset classes, but with respect to investment grade, you can pick up 50 to 60 basis points by going into the muni version of an investment grade credit versus the corporate version of investment grade credit. So, I think they look very attractive relative to, not only from a yield perspective, but also the relative value. Credit quality in municipals is typically much higher. They are typically essential services. Distress levels are much lower. So, from a relative value standpoint, we also think it looks attractive as well.

Mike Taggart:

Yeah, I mean, I think, can you just dig into that a little bit because I think when people hear about, especially high yield, which I want to talk to you about next. You know, there's often a misunderstanding between how municipal high yield is different than corporate high yield when it comes to, like, the average historical default rate.

Miguel Laranjeiro:

Yeah. So high yield, we think, is particularly attractive. When you compare high yield municipals to high yield corporates, the default rate is one seventh of that of the corporate high yield market. So, in other words, the corporate high yield market defaults seven times more than the municipal high yield market.

Mike Taggart:

Not only that, historically and on average and all that sort of stuff, historically speaking, right?

Miguel Laranjeiro:

And not only that, historically speaking, when you look at recovery rates, typically the range of historical recovery rates for the municipal high yield market is between 60 and 90%, where in the corporate high yield market, it ranges between 40 and 60%. So, less times where they get into distress and default scenarios. And when they do, typically there's less volatility and more capital preservation involved in the recovery associated with those distressed criteria.

Mike Taggart:

All right, Miguel, so MFM, the Aberdeen Municipal Income Fund can invest in high yield municipal bonds. And, you were just pointing out that you can pick up some extra spread, some extra yield, right? Municipal bonds compared to corporates right now. Obviously, you know, this fund is trying to provide current, tax-exempt income for its investors. So, how do you consider, in terms of security selection, high yield versus investment grade?

Miguel Laranjeiro:

Yeah, we think high yield is extremely attractive right now, not only with the macroeconomic landscape that I described earlier being relatively stable, but the historical relationship between high yield and its other high yield counterparts look particularly attractive. So, we've been allocating more to high yield. It's where we see value in income focused vehicles such as a closed end fund. We think this is a great place to add income and at the discounts that you're seeing municipal fund closed end vehicles trade at. We think it's a really good opportunity to get involved in an attractive high yield market at levels that are historically inviting and it's a good opportunity for investors.

Mike Taggart:

Excellent. So, let's, can we just kind of delve more into your team's investment process and kind of how credit selection, security selection ties into like the overall macro environment and not just for this environment. Right. But just kind of over time for long, longer term shareholders?

Miguel Laranjeiro:

Yeah, so we take a top-down slash bottom-up approach to our investment making decisions. Not only that, we have an open floor plan. So, we meet biweekly with our economists. We discuss opportunities every day with our analysts, our traders, our PMs, individuals who are not part of the municipal team. Individuals who are involved in infrastructure, individuals who are involved in ESG and environmental mandates. So, we have more of, we have a holistic view on what's going on really in the macroeconomic backdrop, and that informs our target areas, whether we're talking about sector target areas or geographic target areas.

Mike Taggart:

What target areas, would be areas where you either want to lower exposure or increase exposure? Is that?

Miguel Laranjeiro:

Right. So, target areas would be certain sectors, certain parts of the country in some cases, or even certain capital structures. We have open dialogue with our private placements team and they inform us on, you know, parts of the capital structure that they're involved in. And that helps inform our decisions. Same with the equity team. So, I think, you know, really across the landscape, the dialogue across Aberdeen as a whole helps us inform the macro approach and where we're looking to put money to work.

Mike Taggart:

And you mentioned it. So that's kind of the top-down, right? You mentioned it's also bottom-up, which is kind of, right, like we cover everything, right? So, you know, what goes into a bottom-up analysis on a particular security?

Miguel Laranjeiro:

So, what I just described kind of informs where we're targeting our focus in terms of, you know, sector and region and types of structures. Once we've selected a prospective investment, that's when the bottom-up comes in. We utilize our proprietary research together with our analysts and really do a bottom-up analysis. analysis of the socioeconomic landscape of the area we're investing in, debt covenants, their balance sheet metrics, really a bottom-up of how the business works and the surrounding area that enables the business to work. So, there's certain great businesses that have the difficult time surviving in areas where a population is suffering from out-migration. So, I think having that full analysis done is really the only way you can make a good investment decision and have it be sustainable for long periods, which is really what we're looking for as a closed-end fund vehicle, just sustainable income over a long, long period of time.

Mike Taggart:

Right. And so, speaking of sustainable income, so the fund is leveraged, right? Could you talk about, kind of target, target leverage range? And how do you determine the appropriate amount of leverage for the fund at any given time? That sort of thing.

Miguel Laranjeiro:

Yeah. So, leverage is an important tool to really magnify returns, especially in this vehicle. Target leverage somewhere between 30 and 40% is target leverage. I think an active approach to leverage is prudent for those in the closed-end fund space. In the municipal market, we have this vehicle called tender option bonds where you can employ and close leverage really within the span of two weeks. So having those flexible options, which are, that's only a, that vehicle is only available in the municipal market, but having those flexible options enable the management team to employ leverage when they think it suits them best and take off leverage when things become a bit more volatile. Right now, the curve is inverted in the middle part of the curve, but there is a significant spread between the long end of the curve and the short end of the curve.

Mike Taggart:

And the long end is where you invest and the short end is where you borrow. So, it would help support the distribution.

Miguel Laranjeiro:

Right, right. So as that spread widens, it becomes more fruitful to utilize leverage, which has been the trend really over the last two years. It's become wider and wider where the curve was relatively flat a couple of years ago. It's become steeper. So, I think it's a good environment really to add leverage at this point.

Mike Taggart:

Excellent. Well, Miguel, thank you for taking the time today. Appreciate your insights into the Aberdeen Municipal Income Fund. And thank everyone for taking the time to learn more about the Aberdeen Municipal Income Fund.

CEFA:

Thank you for joining us for another episode of CEF Insights. For more CEF insights, videos, and podcast episodes, please visit CEFA.com, your independent source for closed-end fund education data and insights.

Video recorded June 2026.

Disclosure

Past performance is not indicative of future results.

This commentary is for informational purposes only, and is not intended as an offer or recommendation with respect to the purchase or sale of any security, option, future or other derivatives in such securities. Any research or analysis used in the preparation of this document has been procured by Aberdeen Investments or its affiliates for their own use and may have been acted on for their own purpose. The results thus obtained are made available only coincidentally and the information is not guaranteed as to its accuracy. Some of the information in this document may contain projections or other forward-looking statements regarding future events or future financial performance of states, markets or companies. These statements are only predictions and actual events or results may differ materially. The reader must make his/her own assessment of the relevance, accuracy and adequacy of the information contained in this document and make such independent investigations, as he/she may consider necessary or appropriate for the purpose of such assessment. Any opinion or estimate contained in this document is made on a general basis and is not to be relied on by the reader as advice. Neither Aberdeen Investments or any of its agents have given any consideration to nor have they made any investigation of the investment objectives, financial situation or particular need of the reader, any specific person or group of persons. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the reader, any person or group of persons acting on any information, opinion or estimate contained in this presentation. The information herein including any expressions of opinion or forecast have been obtained from or is based upon sources believed by Aberdeen Investments to be reliable but is not guaranteed as to accuracy or completeness. The information is given without obligation and on the understanding that any person who acts upon it or otherwise changes his position in reliance there on does so entirely at his or her own risk. Aberdeen Investments reserves the right to make changes and corrections to its opinions expressed in this document at any time, without notice. Any unauthorized disclosure, use or dissemination, either whole or partial, of this presentation is prohibited and this presentation is not to be reproduced, copied, made available to others. Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in the market value of an investment), credit (changes in the financial condition of the issuer, borrower, counterparty, or underlying collateral), prepayment (debt issuers may repay or refinance their loans or obligations earlier than anticipated), call (some bonds allow the issuer to call a bond for redemption before it matures), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase). Historical data and analysis, should not be taken as an indication or guarantee of any future performance analysis forecast or prediction. Such information is basis and the user of this information assumes the entire risk of any use made of this information. In the United States, Aberdeen Investments is the marketing name for the following affiliated, registered investment advisers: Aberdeen Standard Investments Inc., Aberdeen Asset Managers Ltd., Aberdeen Standard Investments Australia Ltd., Aberdeen Standard Investments (Asia) Ltd., Aberdeen Capital Management LLC, Aberdeen Standard Investments ETFs Advisors LLC and Standard Life Investments (Corporate Funds) Ltd. � Aberdeen Group plc 2026 ID: AA-220626-209669-1 aberdeeninvestments.com